Platform Wars – The Allure and the Illusion of Care

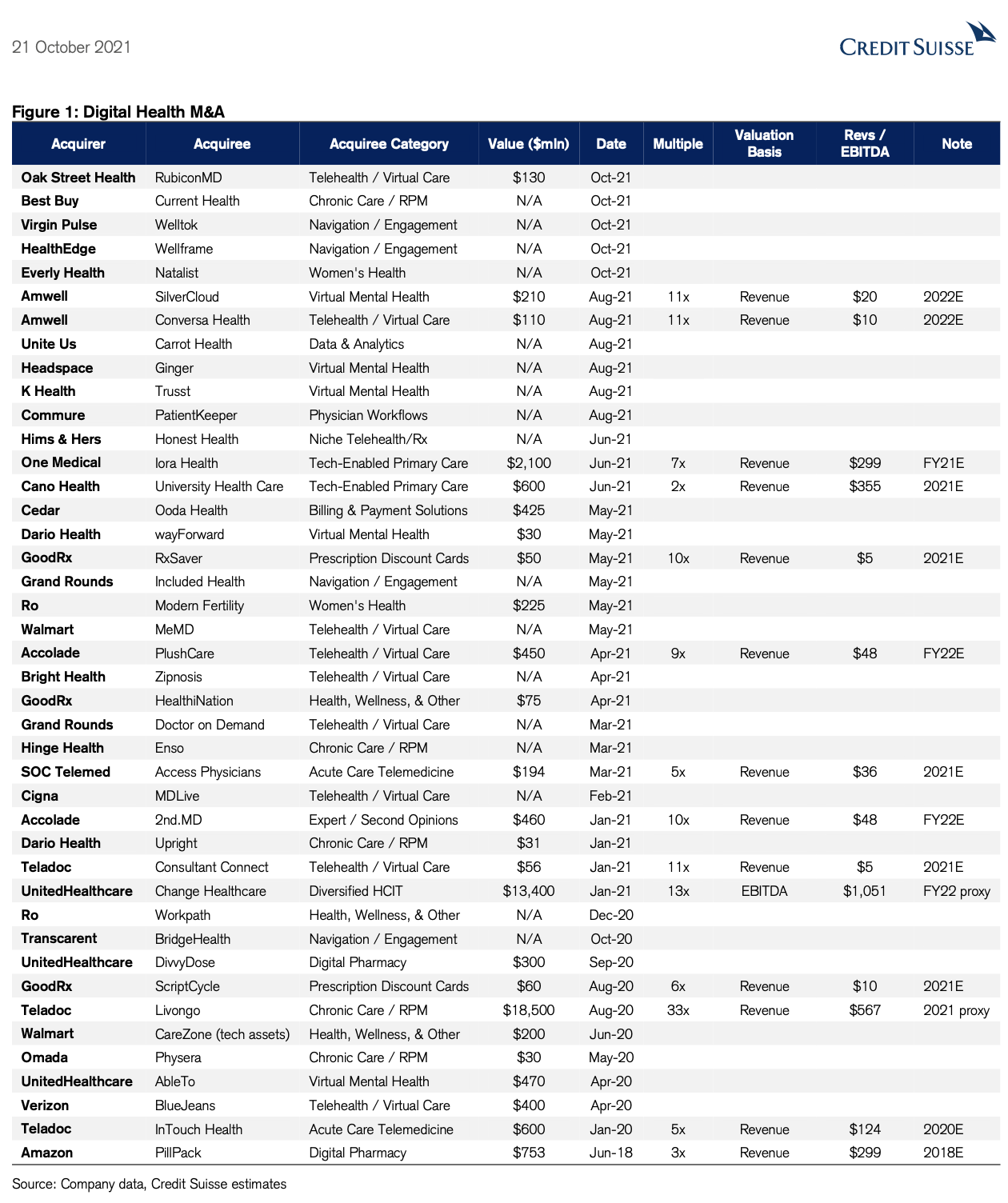

I have the opportunity to read all kinds of health industry reports written from all kinds of angles and perspectives. Some of the best are the investment reports I get from analysts who really understand and know the space, like this recent article from Credit Suisse. It highlights the Great Consolidation taking place in the digital health and tech-enabled primary care delivery sector – I mean, look at the list over the last 14 months:

I usually use the Teladoc / Livongo (August 2020) acquisition as the watershed moment for the surge in interest in the primary care industry. The acquisition represented the point where digital health went mainstream, coincided with the pandemic push into virtual, and was supported by an investment environment where chasing “leveraged” growth was encouraged and expected.

Having recently returned from HLTH, I can tell you that primary care is EVERYWHERE. From the big retailers (CVS, Walmart, Amazon, etc.) to the big tech companies (Google, Apple, Microsoft, etc.), big payers (Aetna, United, Anthem, etc.) and every imaginable startup—and more mutant variants—they are all talking about the fundamental role primary care plays in transforming the costs and impact of healthcare in general, and the need for experimentation. As I have said before—BRING IT! We need all the innovation we can get.

What They Are Saying

That said, there are competing perspectives (aka the Platform Wars) about where this experimentation and innovation in primary care should start from, where its center of gravity should be, and what the focus should be. Case in point: a recent MedCityNews article calling out the non-debate (there wasn’t an actual debate but an aggregation of comments made in earnings calls) highlighted the battling perspectives from prominent CEOs in the space:

From Jason Gorevics, CEO of Teladoc:

“And the truth is that the point solutions, I would say, are really struggling at this point. And I look at all the various players in the market, I wouldn’t probably want to be an onsite, sort of worksite clinic provider at this point since a lot of companies are talking about going virtual. And so that has its limitations. Also, when I look at the navigation companies, I would say, honestly, having been a health plan president, the administrative side of that is fairly low value. We have always focused on making a big clinical impact using our data and our clinical expertise to improve the health of consumers and really focus on the healthcare and not the administrative portion.”

From Raj Singh, CEO of Accolade:

“You need navigation teams. They need to be powered by primary care physicians and mental health specialists who can actually deliver the care and we’ve done so in a virtual model that says, ‘You are going to see a primary care physician, they are going to stay with you through your journey.’ It’s not transactional, like a Teladoc, for example. If you need an expert consult, that is going to be human. There’s going to be a mental health professional in everyone of your care teams. So we are going to be human-oriented, data-driven, and measurable.”

From Glen Tulman, CEO of Transcarent:

“I am not as kind to navigators because I think navigators are yet another step in this process and you can’t navigate a broken system. So the first thing is you can’t navigate a broken system. Hospitals are not the problem, providers are not the problem. They provide the care. We need two sides of the equation. We are the health consumers and we are the real payers. It’s us and the folks we work for. Then on the other side are the providers. That’s all that is necessary. Good software takes the middle out. That’s where the friction is. That’s where the challenges are. That’s where all the cost is. And, that’s sucking up all the profit today.”

Why They Are ALL Wrong

I have written extensively in the past about what I consider to be the solution to the healthcare problem in our country (Here, Here, and Here). Starting from first principles, how would you even design a new primary care system? Would you start with virtual only? Would you have navigators in isolation? Would you attempt to bypass everything with software that removes the systemic friction? What these publicly traded company CEO’s are presenting is really a choice of how to organize your healthcare delivery—is it around technology, around navigation, around payment? Or rather, should it be around the actual delivery of care?

I believe the choice is clear—you should organize your new health system around the entity that actually is closest to patients, that has their trust, that is in touch (literally), and is always connected. That’s the Medical Group. It’s where the insights generated are delivered in real time and in context directly from your trusted provider (no intermediaries necessary!); where the care team surrounds you with support; where the navigators are actually embedded as part of the care team; where your team walks with you in the most confusing, complex, and costly parts of your healthcare journey; and where that team is always proactively measuring, monitoring, and partnering to improve your health.

This isn’t your grandpa’s disjointed, disengaged medical group—this is the future we need (metaverse-enabled coming soon!).

The allure and the illusion of primary care

What I see from the current industry narrative is the allure of care—“Hey, we can do this virtually only,” or “Hey, my chatbot will intervene at the right point,” or “Hey, my AI magic unicorn thingamabob will bolt onto your cerebral cortex and send you the signal,” and other related alternative realities. But, I believe this thinking leads to an illusion of care that the industry should be wide-eyed about, including patients who should be asking questions, pushing back and demanding real care on their terms which leads to optimal health. More fragmentation by more tech, further distance and displacement of real relationships, and more noise and nonsense without addressing the actual delivery of care by actual providers is a problem that I think should be put front and center of the conversation.

Instead of all this fancy and fanciful technology replacing the actual care by a provider, why not just have the care providers themselves be more capable, more technologically advanced, and more “powerful” in their ability to influence the care, the health and the outcomes of their patients? Why not start with the Medical Group as the foundation to be the organizing catalyst to re-architect the system and make sense of all of these innovations? I believe a next gen, capable Medical Group is THE answer—an awesome, technology-enabled experience that also involves real humans who engage in real relationships with a care team that can literally help you fix and resolve your problem (again, no intermediaries necessary!). We see a growing number of people, payers, and even providers who want – and shortly will demand – to practice and receive care in this way.

Beyond the Platform Wars

The platform wars will continue to play out in both the public and private marketplace. Employers, payers, and others should be paying attention because market forces are pushing a proverbial “arms race”. You can see the Navigators expanding, merging, and acquiring to be more complete and more competitive. You can see Technology-centered companies expanding reach, scope, services, and related capabilities. And, you can see Care Delivery innovators like Crossover preparing to enter the arena with our Full Stack Primary Health. In this new world, I am going to bet on the most trusted, most capable entity that actually delivers a comprehensive, integrated, coordinated, and accountable Primary Health platform while achieving cost, quality, experience, and engagement expectations.

No magic, no illusions—just the real deal care delivered by tech-enabled care teams who understand the powerful potential and impact of the human touch. It’s how care, and health, should be.

Leave a Reply